In Chemung County, a homeowner whose property sold for $40,000 pays 72% more

in property taxes per dollar of actual value than a homeowner whose property

sold for $300,000. This is not an accident. It is the direct result of a frozen

assessment roll.

The Simple Version

Before the charts and the ratios, here is what is actually happening.

The county has to decide how much every house is "worth" so it knows how much

to charge in property taxes. An assessor sets those values. Whatever number

the assessor puts on your house — that's what you pay taxes on.

The assessor in Elmira hasn't really updated those numbers in a long time.

When houses actually sell, we find out what they're really worth —

because a real person paid real money for them. So we can compare: what did

the assessor say the house was worth versus what did someone actually

pay for it?

Here's what the data shows. Cheap houses — the ones in the

struggling neighborhoods, selling for $30,000 or $40,000 — are assessed at

more than people actually paid for them. Those owners are paying

taxes on value that doesn't exist. Expensive houses are

assessed at far less than what people paid. Those owners get a big discount.

The result: a family in a $40,000 house pays 72% more in

property taxes per dollar their home is actually worth than a family in a

$300,000 house. Same tax system. Very different deal.

Why? Because houses in nicer neighborhoods went up in value over the years,

but the assessor never updated the numbers to keep up. The cheap houses in

struggling neighborhoods didn't go up in value — so their numbers stayed

roughly accurate. And it gets worse every year that the roll stays frozen.

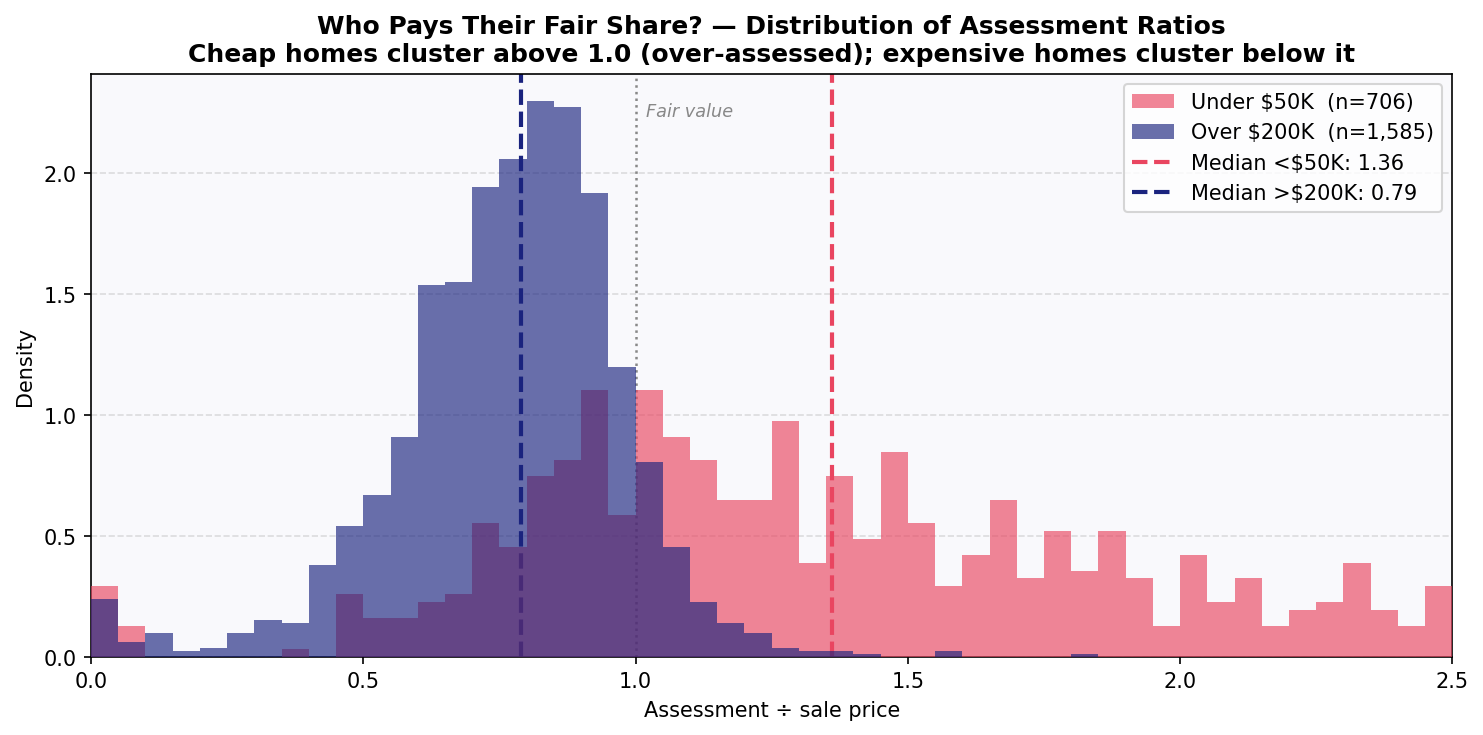

The Assessment-to-Sale Ratio

When a property sells, we can compare what the assessor said it was worth to

what a willing buyer actually paid. That ratio should be close to 1.0 for a

fair assessment. In Chemung County, it isn't — and the gap is not random.

1.36Median ratio — homes under $50K assessed at 136% of sale price

0.43Median ratio — Elmira homes $125–150K assessed at 43% of sale price

0.79Median ratio — homes over $200K assessed at 79% of sale price

1.72×Tax burden gap — cheap vs. expensive per dollar of actual market value

A ratio above 1.0 means the assessed value exceeds what the property actually

sold for — the owner is paying taxes on phantom value. A ratio below 1.0 means

the property is under-assessed — the owner pays less than their share. In a fair

system, both would cluster near 1.0 regardless of price. In Chemung County,

cheap homes cluster above 1.0 and expensive homes cluster below it.

This analysis uses 6,491 arm's-length single-family sales

recorded in Chemung County between 2018 and 2025. Arm's-length sales are

transactions between unrelated parties at fair market value — foreclosures,

family transfers, and quitclaims are excluded. The data comes from the New York

State ORPTS SalesWeb system.

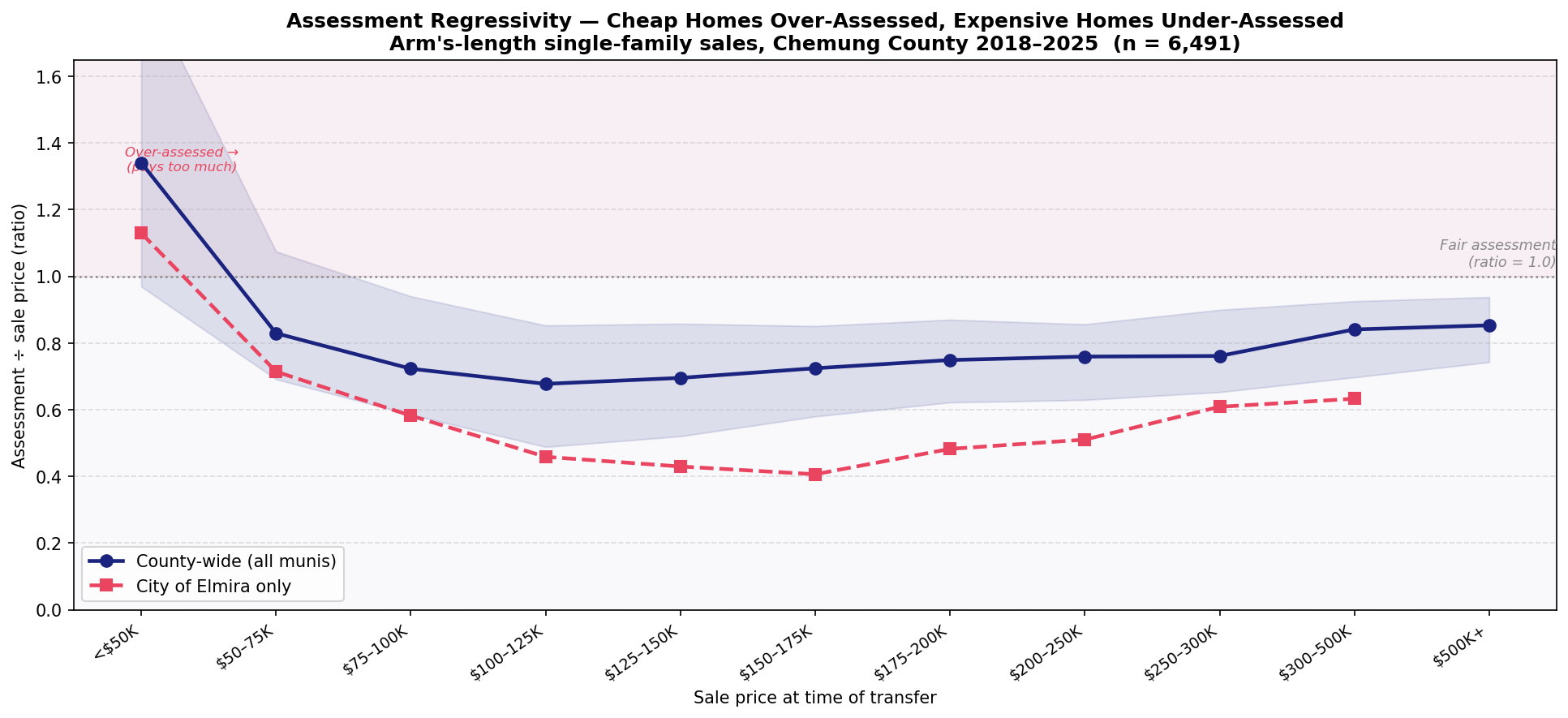

The J-Curve

Plot assessment ratio against sale price and a pattern emerges: over-assessment

at the bottom, under-assessment in the middle, partial recovery at the top.

The shape is consistent with what researchers find in cities across the country

that haven't reassessed in decades.

The county-wide J-curve shows the cheapest homes — those selling under $50,000 —

carrying a median ratio of 1.36. These are the houses in the most distressed

neighborhoods, the ones most likely to be owned by people with the least

political power and the least ability to appeal their assessments. They are, on

average, paying property taxes on value that does not exist.

The City of Elmira's curve is steeper. An Elmira home that sold for $125,000

to $150,000 carried a median assessment ratio of 0.43 — assessed at less than

half its actual market value. The frozen assessment roll has allowed decades of

market appreciation to go uncaptured in Elmira's tax base while leaving the

cheapest properties stuck near their assessed values, which haven't fallen

as fast as the neighborhood conditions that drove prices down.

The mechanism is straightforward: when a city stops reassessing,

assessments drift away from market values at different rates in different

neighborhoods. Neighborhoods that have appreciated (even modestly) see their

assessments fall further below market. Neighborhoods that have declined see their

assessments stay closer to — or exceed — actual value. The result is a transfer

of tax burden from appreciating areas to declining ones, which in Elmira means

a transfer from wealthier to poorer households.

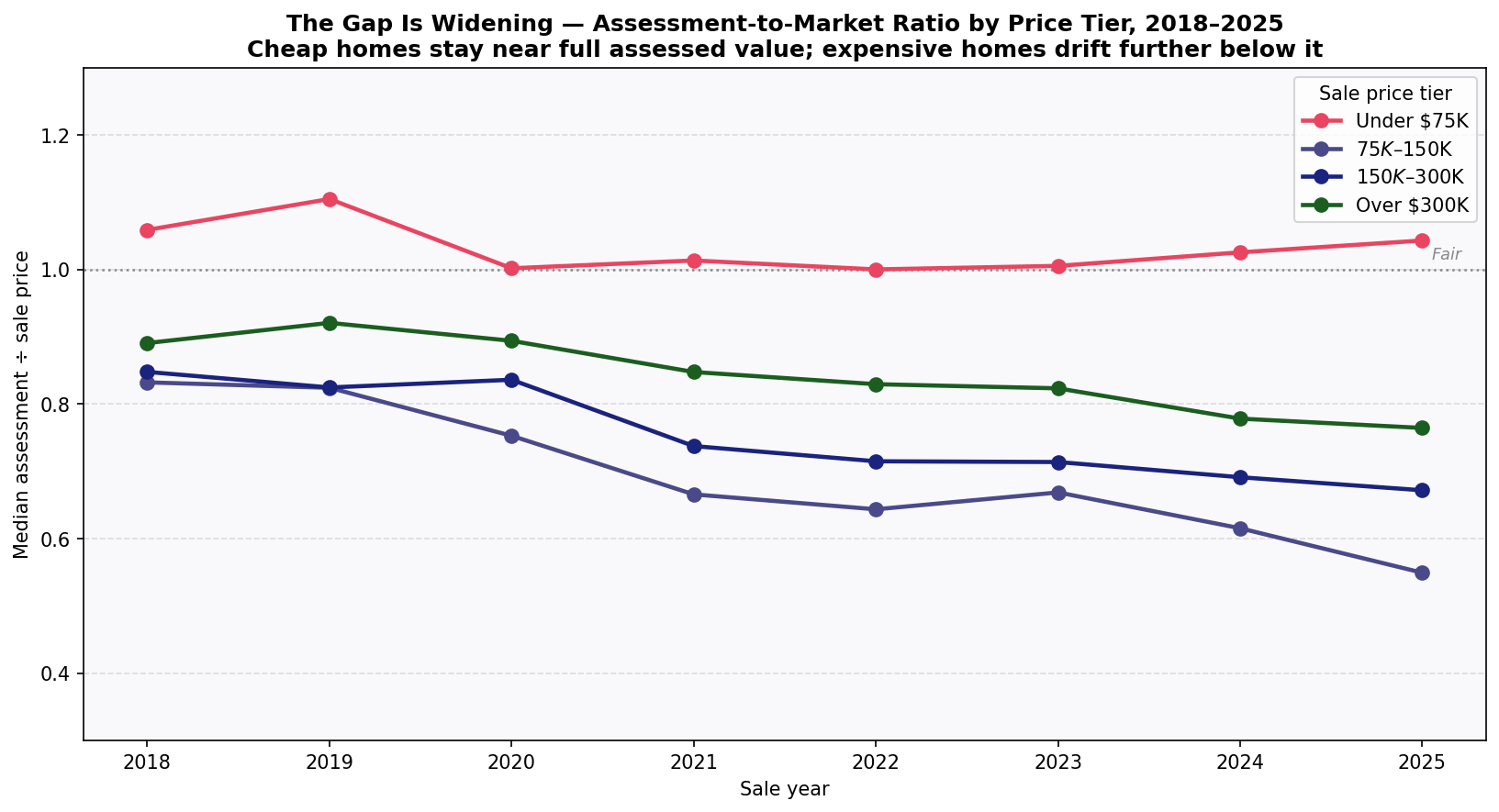

The Gap Is Getting Worse

Year-by-year data from 2018 to 2025 shows the assessment ratio for mid-range

and expensive homes falling steadily while the ratio for cheap homes stays near 1.0.

Without reassessment, this trend continues indefinitely.

In 2018, a home selling in the $75,000–$150,000 range carried a median ratio

of about 0.83 — assessed at 83% of market value. By 2025, that same price range

had a median ratio of 0.55. The gap between cheap homes (ratio holding near 1.0)

and mid-range homes (ratio falling year over year) has nearly doubled in seven years.

This is what happens when a housing market moves and assessments don't. Post-pandemic

home price appreciation hit Chemung County the same way it hit the rest of the

country — median sale prices for arm's-length single-family transactions climbed

significantly between 2020 and 2024. The assessment roll didn't follow. The result

is an ever-larger subsidy for properties that have appreciated, paid for by

properties that haven't.

The only corrective is reassessment. The equalization rate adjustment the state

applies — which produced the apparent jump in Elmira's "full value" figures in

2023 — adjusts how the state measures the roll for aid and apportionment

purposes. It does not change a single property's assessed value. No one's tax

bill changes because of the equalization rate. Only a actual citywide reassessment

resets individual assessments to current market value.

Elmira Specifically

The city's regressivity pattern is sharper than the county average —

and the stakes are higher, given the city's poverty rate and tax burden.

Among the 1,699 arm's-length single-family sales recorded in the City of Elmira

between 2018 and 2025, 17.7% involved a property assessed at

more than its sale price. These are predominantly in the lowest price tiers —

homes under $50,000 — in the city's most economically stressed neighborhoods.

The households in those homes are disproportionately renters (whose landlords

pass property taxes through in rent) or low-income owners who have limited

options to appeal or move.

Meanwhile, properties at the middle and upper end of the Elmira market are

dramatically under-assessed. A home selling for $130,000 in Elmira in 2024

typically carried an assessed value under $60,000. The owner pays taxes on

$60,000 worth of property while living in a $130,000 house. The effective tax

rate per dollar of actual value is less than half what a neighbor in a $40,000

assessed property pays.

This is not a story about the rich avoiding taxes. Most of these properties are

modest working-class homes. The regressivity isn't driven by mansions being

under-assessed — it's driven by an entire housing market appreciating away from

a frozen assessment roll, unevenly, in ways that happen to follow income and

neighborhood lines.

Assessment regressivity is not unique to Elmira. It has been

documented in Chicago, Detroit, Philadelphia, and dozens of other cities with

infrequent reassessment. The pattern is consistent enough that the academic

literature calls it a structural feature of low-reassessment systems, not

administrative error. The Chemung County data fits the pattern precisely.

Charts

Three views of assessment regressivity: the J-curve shape, the trend over time,

and the distribution of ratios at the top and bottom of the market.

All data: arm's-length single-family sales, Chemung County 2018–2025 (n = 6,491).

The J-Curve — Assessment Ratio vs. Sale Price

County-wide (blue, with IQR band) and City of Elmira only (red dashed).

The horizontal dotted line is a fair assessment (ratio = 1.0). Properties

above the line are over-assessed; below it, under-assessed. Elmira's curve

is steeper across nearly every price tier.

The Widening Gap — Ratio Trends by Price Tier, 2018–2025

Cheap homes (red) hold near 1.0 while mid-range and expensive homes drift

further below fair value each year. The gap between the cheapest and most

expensive tiers has nearly doubled since 2018.

Who Pays What — Distribution of Ratios

Cheap homes (red, under $50K) cluster above the fair-value line; expensive

homes (blue, over $200K) cluster below it. The vertical dashed lines show

the median for each group — a 72% gap in effective tax rate per dollar

of actual value.

What Changes This

Reassessment. That is the only mechanism that corrects assessment regressivity.

When a city reassesses to current market value, every property's assessed value

is reset to reflect what it would actually sell for today. The ratio distribution

tightens around 1.0. The effective tax rate per dollar of value equalizes.

Reassessment is often described as a tax increase on long-time homeowners — and

for some it is, if their neighborhood has appreciated. But the framing obscures

what's actually happening: under the current system, those same long-time

homeowners have been receiving a subsidy, paid by their neighbors in cheaper

properties who have been over-assessed. Reassessment doesn't raise taxes — it

reallocates them to reflect actual values.

The Elmira page models what citywide

reassessment would mean for the distribution of assessments and who would see

their bills change. The Why It Matters page

explains why reassessment hasn't happened despite the evidence, and who benefits

from the status quo.

Method: 6,491 arm's-length single-family (class 210) sales in

Chemung County, 2018–2025, from NYS ORPTS SalesWeb (data as of May 2025). Each sale's

assessment-to-sale-price ratio = assessed value ÷ sale price. Sales below $10,000 and

ratios above 5.0 are excluded as likely data errors or non-market transfers. The

headline gap compares the median ratio for sales under $50K (1.361) with sales of

$200K or more (0.790): 1.361 ÷ 0.790 ≈ 1.72×, i.e. 72% more tax per dollar of value.

The regressive pattern this measures is well documented in the assessment literature

(e.g. Berry 2021 on Chicago; Avenancio-León & Howard 2022).